Cost Inflation Index (CII) for FY 2025–26 Set at 376

Context: The Central Board of Direct Taxes (CBDT) has notified the Cost Inflation Index (CII) for Financial Year 2025–26 as 376, up from 363 in FY 2024–25 — a 3.58% increase.

Purpose:

-

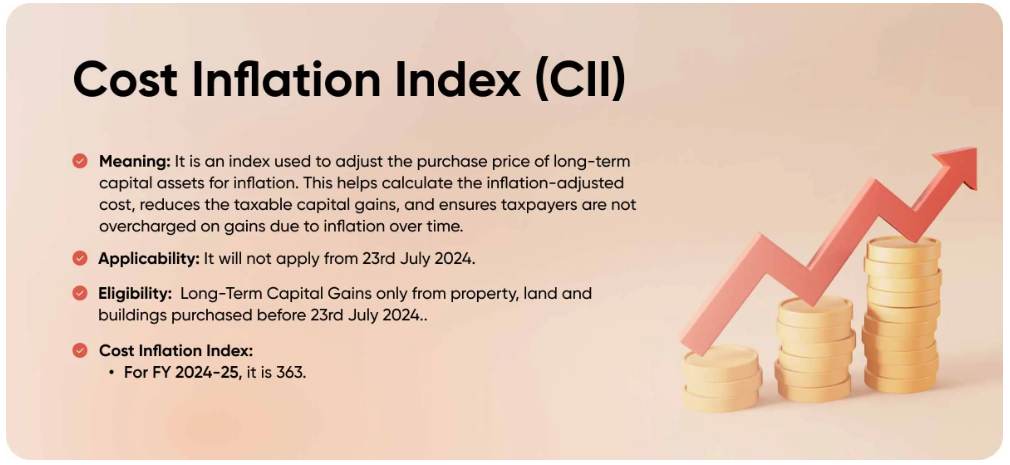

CII helps calculate long-term capital gains (LTCG) on assets like land, buildings, trademarks, patents, securities, etc.

-

It adjusts the purchase price for inflation (called indexation), thereby reducing the taxable gain and tax liability.

Applicability:

-

This new index will apply to Assessment Year 2026–27 onwards.

-

It is applicable only for assets acquired before July 23, 2024.

-

For land/building bought before that date, taxpayers have a choice:

-

12.5% tax without indexation, or

-

20% tax with indexation using CII.

-

Key Implications:

-

Lower LTCG taxes for those selling pre-July 23, 2024 assets, thanks to the higher CII of 376.

-

No CII benefit for assets acquired after July 23, 2024, as per Finance Act 2024.

-

For debt mutual funds, indexation was already removed by Finance Act 2023; now taxed as per income slab (up to 35.8%).